The nightmare that more and more cities and states are facing is the pension (liability) nightmare, and no one really wants to talk about it; and if a city is struggling to make those pension payouts, they probably don't want you to know about it.

The next time you talk to your local politician, ask them:

1. How much do we have in the pension fund now?

2. How many former employees are receiving pensions now, and what is the yearly payout for each?

3. What city employees are eligible to receive a pension?

3. What city employees are eligible to receive a pension?

4. Where are we getting the money to fund these pensions?

5. Where did we get the money (source of funding) to pay pensions last year and the year before that?

6. How much do we have to payout for the current year, and each year after that for the next 20 years?

7. What is the average pension payout per person per year?

8. When can the employee begin to receive a pension (after how many years of service)?

9. Are we in the red (underfunded) or black, and if underfunded, by how much, and what are we going to do to fully fund it?

10. What happens if we can't make the pension payments?

11. Can levies be used to help make these pension payouts?

12. Can tax money that is supposed to be used for services/salaries, legally be diverted to fund pensions?

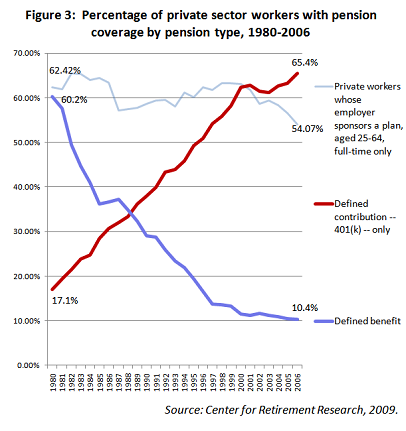

Many Americans look at the crisis in Greece and shake their heads wondering how it is possible for an entire country to derail the future of its younger generation. One big problem in Greece was massive government liabilities funding very generous pensions. Yet this came at an enormous cost. The US is facing a different crisis but the markets have already responded over the last few decades. In the early 1980s, roughly 60 percent of private sector workers had a pension. Today, it is down to 10 percent in the latest data and will likely continue to decrease. For young Americans entering the workforce, the self-funded 401k is likely the only path to having a nest egg and any sort of retirement. This is why so many people get angry when they hear about some in California that retire in their early 50s pulling in annual pensions of $100,000. Over 20 to 30 years this can range from $2 to $3 million of payouts. And we wonder why states face a $3+ trillion funding gap with pensions. Are we simply ignoring another looming crisis?

The shift away from pensions

While the stock market inches closer to a previous peak, the shift with pensions has been rather dramatic:

Only about 10 percent of private sector workers have the opportunity for a pension. This of course is likely lower given the trend above. While many might think this is an issue to deal with in the future the crisis is very real:

“(The Atlantic) In addition, states have funded only about 80 percent of their pension liability, leaving a $3.32 trillion funding gap. Ohio and Rhode Island are in the worst shape, having underfunded their pensions by almost 50 percent of their gross state product. Other liabilities, such as retiree health and dental insurance, also are underfunded. City governments similarly are plagued by underfunded pensions, with Los Angeles underfunding its public pension liabilities by $3.53 billion, with an additional $2.43 billion owed for other employment benefits such as healthcare. As of June 2009, New York City public pension programs had liabilities that exceeded their assets by $39.9 billion with an additional $65.5 billion owed for other benefits.

So both the private and public components of the U.S. pension system are under severe strain, as the Great Recession combined with pre-recession patterns of rising inequality and a diminishing social contract have taken their toll. With fewer workers covered by pensions, this leg of the three-legged stool of retirement security is too short — and growing shorter.”

This is incredible. Guess who will cover this gap? The taxpayer. And of course, we are talking about massive payouts for many. In California, over 18,000 people collect pensions of over $100,000.

Read the rest HERE"

PS:

No comments:

Post a Comment